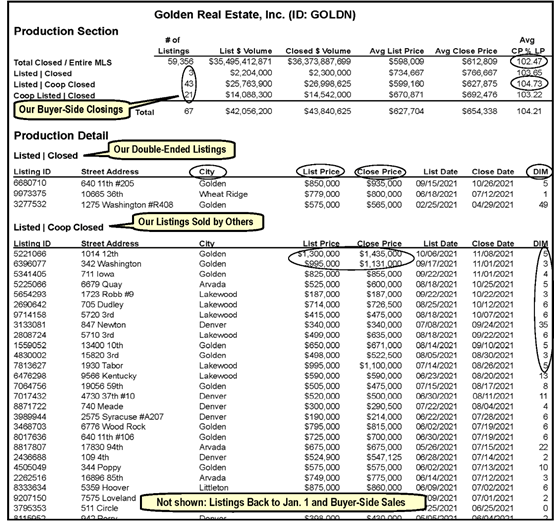

The MLS printout for Golden Real Estate below shows the information that can be gleaned about individual agents and their brokerages. I’m showing our company report, but I could have shown my personal report. This print-out shows our production since Jan. 1st of this year.

The Production Section at top summarizes the report, showing that we had 46 listings since Jan. 1st, three of which we sold ourselves. We had 21 buyer-side closings. The right-hand column shows the average of closed price (CP) to listing price (LP) — 102.47% for all MLS sold listings but much better for Golden Real Estate’s sold listings — 104.73%.

In the Production Detail section, the right-hand column shows how many days each sold listing was on the MLS before going under contract. Notice there are no zero days in MLS (“DIM”) because every listing was exposed to the full market so it would attract the most buyers, and yet there are few listings that took over a week to sell.

The “City” column lets you know where the agent (or company) does most of its business. The “List Price” and “Close Price” columns are also instructive. I’ve circled the two most recent sales as examples of how much above the listing price we sold those listings, thanks to our “auction style” of handling multiple offers, as opposed to the “highest and best” approach of most listing agents. It takes more work, but yields better results (a higher price) for our sellers.

This is not to suggest that an agent’s production is the sole criterion you should consider in choosing your listing agent. However, we learn from experience, which comes from actual transactions, not from years in the business. An agent with only five years’ of licensure but who does a dozen-plus transactions a year can be more “experienced” than an agent who has done a couple transactions a year over a 20-year career.

And let’s not forget about testimonials. Ask for them, and look for online reviews, too. We like www.RatedAgent.com, because it only displays reviews solicited from actual clients following a closing, so the reviews can’t be phonied up or altered in any way.

The government’s supervision of lenders has changed the way that home loans are made. Once you select your lender, you will be interacting with multiple people. Understanding who the “players” are is important.

I asked Jaxzann Riggs, owner of The Mortgage Network to describe those players..

The Loan Originator/Loan Officer

Sometimes called a “loan originator” or “loan officer” (LO) this is your team manager. Your LO will typically be your first contact with the lender. The LO decides if your income, assets, and credit will allow you to obtain the financing you need. The LO will be an educator and your advocate. He/she will manage the overall progress of the application, making sure that deadlines agreed upon by you and the seller are honored.

The Processor

The processor is the player tending to your loan application as it winds its way from application to closing. Your processor will request documentation from you that supports the information that you and the LO have put into the application for the loan. Their job is to organize your documents so that they paint a clear picture of your ability to repay the loan. The loan processor is the go-between between the borrower and underwriter.

The Appraiser

The appraiser will create a report that assesses the home’s market value to ensure that the amount of money requested for the loan will be acceptable to FNMA or FHLMC. The appraiser confirms the home’s dimensions, examines amenities, and evaluates the overall condition. He/she examines the records of comparable properties, ideally ones in the same neighborhood that have sold recently. Based on this information, the appraiser arrives at an opinion of how much your property would sell for if you put it on the market. This opinion assists the underwriter, along with your income, assets, and credit history in deciding how much it will lend you and on what terms.

The Underwriter

Think of the underwriter as the final word. FNMA and FHLMC are quasi-governmental agencies that set underwriting standards which lenders must follow. After reviewing your credit history, assets, the size of the loan, and the appraisal of the home, it is the underwriter who will decide whether your application meets government standards and either approve or decline the application. If they decide that your credit profile or application does not meet FNMA/FHLMC standards, they may deny your mortgage or require a larger down payment. Underwriters have discretion in the approval decision and, while they are the “gatekeeper” for the lender, they typically will look for ways to approve the loan.

The Closer

While not obvious, there are two “closers” working on your loan team. The title company’s closer must coordinate with the lender’s closer to reconcile the numbers associated with the loan and real estate transaction. The title closer will be presenting the lender’s final documents for your signature on the day of closing. The closing package includes the final loan application, loan estimate and closing disclosure, title insurance documents, deed of trust, bill of sale, affidavit of title, tax documents, etc. While they start their work at the beginning of the transaction, their work is not finished until all the documents that you sign at closing have been recorded with the county.

The Most Valuable Player (MVP)

The most important player is YOU. Your LO and Loan Processor will not ask you for documentation unless they know that it will be required by the underwriter. The more responsive you are to their requests, the faster the loan will be approved and the lower your stress level will be during the process.

Do you have other questions about the mortgage process? I recommend calling Jaxzann at 303-990-2992.

Recent experience with my listings has caused me to rethink recommendations I’ve made in the past about fixing up a home before putting it on the market.

Despite a moderating seller’s market, two recent listings went under contract for way above their listing prices, and I think it was because of the effort and money that was expended on dressing them up for sale.

In previous columns I have said you don’t need to do much to sell a home. Only fix “eyesores,” I wrote. If the carpet is old but not damaged or rippled, just have it professionally cleaned, don’t replace it.

My most recent seller, however, spent significant time and money dressing up their home before putting it on the market, and I think it paid off. The home was listed at what the comparable sales suggested it should sell for, but it attracted 12 offers and ended up going under contract in five days for 20 percent over the listing price.

The new carpeting was well chosen and beautifully installed. The seller followed our stager’s advice to the letter. The deck was re-stained. The concrete flatwork which had settled was mud-jacked. Windows were washed and screens labeled and put away. I asked the seller to describe all they had done over several months, and it’s super-instructive. Here’s a link to what they wrote.

Another effort — by me — really paid off, too. The narrated video tour with drone video which we put on YouTube and linked to the MLS and our website was so effective in showing off the home that a buyer from the East Coast submitted the winning offer without seeing it in person. That’s because our videos simulate an actual showing, starting out front (just like a real showing) and going through the home and into the backyard, narrating all the time.

As I wrote in a previous column, we are amazed that more agents don’t shoot live action narrated videos. They’re easy to do once you get the knack of it, and they cost nothing to create and edit if the listing agent does it himself. And who better than the listing agent to “show” a listing?

Come on, dear colleagues, get with the program. It can pay off for you as it pays of for Golden Real Estate agents week after week!

In November 2019 the National Association of Realtors (NAR) created its Clear Cooperation Policy (CCP) designed to end the practice of “pocket listings.” A pocket listing is one which an agent keeps in his or her “pocket,” hoping to sell it himself instead of giving other agents the opportunity to sell it. The incentive is financial. Roughly half the listing commission goes to the agent who sells a listing. If an agent sells the listing himself, he/she gets to keep the entire commission.

The term “clear cooperation” is a reference to the purpose of the MLS, which is “cooperation and compensation.” Every MLS member agrees to cooperate with other MLS members, allowing them to sell their listing. And every listing specifies the compensation which the buyer’s agent will receive — typically 2.5 to 2.8 percent in our market.

You can read the three previous articles I’ve written about this policy at www.JimSmithColumns.com. Those articles (in Nov. 2019, Feb. 2021, and Aug. 2021) document the creation of the CCP and its subsequent implementation by REcolorado, our MLS. The deadline set by NAR to do so was May 1, 2020.

My August 12, 2021, column described how our MLS is fining agents $1,500 for a first offense when they fail to put a listing on the MLS within one business day of promoting it outside their own office in any way — online, in print or via a sign in the ground.

One would think that with such a big penalty the number of homes selling with zero days on the MLS would have declined, but in fact they have increased. I didn’t realize that until I read a Nov. 3rd article from Inman.com which quoted a study by Broker Resource Network (BRN). The study pulled data from 24 multiple listing services comparing the number of homes sold with zero days on MLS during the 12 months before and after the May 1, 2020, implementation date.

“In every market reviewed across the United States, brokerages recognized double and triple digit increases in Zero Days On Market listings across firms of all sizes and business models,” the report said. These were figures for big brokerages, not the full MLS.

So I checked REcolorado statistics to see what our full-MLS statistics are for homes sold with zero days on the MLS. I found that there were 2,225 such closings reported in the 12 months before May 1, 2020, and 2,769 reported in the 12 months after May 1, 2020 — a 24.4% increase.

To discover the longer trendline, I looked at several half-year periods going back to 2018. In the last 180 days (as of this past Sunday), there were 1,677 closings of resale residential listings recorded on REcolorado with zero days on MLS before going under contract.

During the same 180 days of 2020, there were 1,295 such closings, making this year a 29.5% increase over last year. The number in 2019 was even lower — 1,077. In 2018 it was not much different — 1,104.

What could account for this counter-intuitive increase?

One explanation might be the explosion of the seller’s market during the pandemic, which really took off simultaneously with the implementation of the Clear Cooperation Policy (and the pandemic surge).

One way to assess the seller’s market is to measure how many homes went under contract after 4 days on the MLS during those 12 months before and after May 1, 2020, and the median ratio of sold price to listing price for those listings.

During the 12 months before the implementation of the CCP, there were 4,563 closings of listings which went under contract in 4 days, and the median ratio of sold price to listing price was 1.0019. During the 8 months after May 1, 2020, there were 4,896 such closings, and the median ratio was 1.01299. Another 2,840 such closings took place during the remaining 4 months of the 12-month period after May 1, 2020, and the median ratio for them was 1.05157. Clearly, the seller’s market was accelerating. It makes sense that more sellers might receive offers they “can’t refuse,” and that listing agents might encourage them to accept those offers.

There was an important loophole created when the CCP was implemented by REcolorado and perhaps by those 24 other MLSs. That loophole is called the “office exclusive,” which allows any brokerage to promote an off-MLS listing within the brokerage, so long as there is no advertising of any kind on social media or in print and no sign in the yard — the definition of a pocket listing.

This policy greatly favored large brokerages which could have hundreds of agents in a dozen or more offices, to promote new listings internally with the additional incentive of keeping the full commission of each transaction within the brokerage.

If this loophole were to be closed, there would probably be far fewer closings with zero days in the MLS — and sellers might get more money for their homes by having them exposed to more competing buyers.

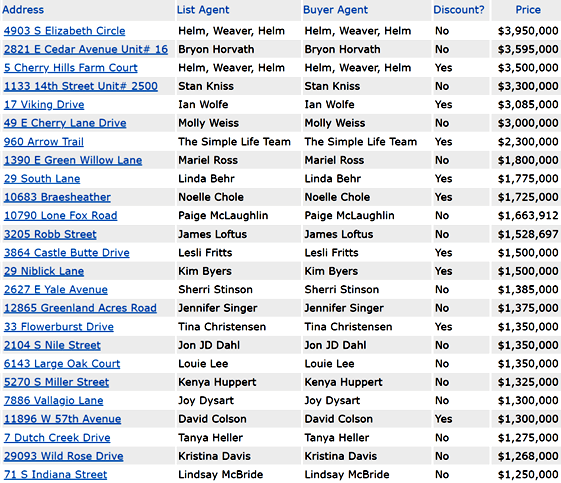

As I mentioned above, a listing agent profits from keeping a listing off the MLS, because it increases the chances of selling the listing himself and thereby greatly increasing his/her commission. Of the 100 homes on REcolorado which sold for $1.25 million or more in the last 180 days with zero days on the MLS, 25% of them were double ended (see list below), and only 9 of those 25 listings reduced the commission paid by the seller because of their listing agent’s windfall. (The agents at Golden Real Estate always discount our commission when we double-end a transaction.)

D0uble-Ended Sales On REcolorado Over $1.25 Million – Last 180 Days, Showing Whether Seller Got a Discounted Commission

By contrast, of the 100 highest priced homes ($1,575,000 and over) which sold after 4 days on the market, only 2% were double-ended. Whether or not you call it “greed,” the agents who kept their homes off the MLS greatly profited from it — and the sellers paid the price by not exposing their homes to all potential buyers.

Another recent article from Inman reminds us that Fair Housing was one of the reasons the Clear Cooperation Policy was introduced. A blog post on REcolorado also makes this point. The reasoning is that if a home is sold privately without being exposed to all buyers on an MLS, then it is more likely to be sold within the same demographic. Thus, pocket listings are inherently discriminatory against minority groups, whether they be racial or, for example, LGBTQ.

I’m sure that these articles and the studies behind them, including my own analysis of REcolorado statistics herein, will lead to some discussion locally and nationally about how to tweak the Clear Cooperation Policy so it is more effective and less counter-productive, which it clearly has proven to be. I do not believe, however, that the Clear Cooperation Policy will be scrapped, because its stated intention is clearly good public policy.

Sellers: Insist that your home is put on the MLS so that all interested buyers have the opportunity to see it and participate in a bidding war that nets you more money.

Disruption is happening in every industry, spurred on primarily by internet-based technology. Amazon is disrupting brick and mortar retail. Uber and Lyft have disrupted the taxi industry. Tesla disrupted the auto industry’s dealer model. Travel agents have suffered from online ticket sales by airlines, cruise lines and related businesses.

Now companies like Zillow, Open Door, and OfferPad are disrupting the real estate industry with their “iBuyer” model.

But those and other disruptors have not killed off the older business models. They are grabbing market share, but of an increasing market. You can expect to see brick and mortar retail stores, taxi companies, travel agents and, yes, traditional real estate brokerages such as Golden Real Estate thriving for years to come.

We ourselves have not suffered from these disruptors. Indeed, while 2020 and 2021 have seen huge growth by these new real estate enterprises, they have also brought record growth for our brokerage and other traditional brokerages, and it is easy to see why.

Buying and selling a primary residence is typically the biggest financial transaction we all deal with. Yes, buyers increasingly utilize the internet to search for homes, but they end up calling us to see them. Sellers also use the internet to monitor the market — many taking advantage of the MLS alerts that we set up for them — but they want someone they know and trust to bring their real estate savvy to bear in listing and marketing their home when it’s time to sell.

The “full-service” real estate agent is being redefined, and I like to think that my broker associates and I epitomize that evolution. Some of the services we provide can not be obtained from those other companies.

Full service goes beyond providing our free moving truck, moving boxes and packing material, which we’ve been doing since 2004. Here are some other services you can expect from us.

We have an in-house handyman who can help with preparing a home for market, such as repairing drywall damage, washing windows, and doing light plumbing and light electrical tasks such as installing a new toilet, faucet or light fixture. He’s also there to address many of the issues which arise from the buyer’s inspection. And he’s also there if needed to drive our truck for moving, or even for a dump run or for taking a load of possessions to Goodwill or Arc.

We also have a certified home stager who provides our sellers with a free consultation to help their home show its best.

You’re familiar by now with how we create narrated video tours of each listing, including drone videos, but we also serve out-of-state buyers by shooting videos of other agents’ listings that interest them. Last June I did that for a Minnesota couple who felt they had “seen” an Arvada home well enough through my narrated video tour of it to go under contract, not visiting the home in person until they came for the inspection.

Speaking of inspection, experienced agents like us from a traditional brokerage can be counted on to recommend a good inspector who has a track record with them. Other specialists we know and trust — giving our clients the comfort to employ them — include estate sales companies, structural engineers, electricians, plumbers, HVAC companies, and more. The real benefit from these trusted vendors is that they will make sure you’re satisfied with their work, because they want to be referred to future clients.

“Full service” also implies availability and responsiveness. My broker associates and I are available 7 days a week, and we answer our cell phones on evenings and weekends. Although I have associates who can be my “boots on the ground” when I go on vacation, I take my cell phone (and laptop) with me, and I answer it when it rings.

Often we provide service for which we don’t expect or receive any compensation. For example, this past Sunday I got an inquiry from a man who had inherited his mother’s house and wanted an appraisal for tax purposes. I explained that only licensed appraisers can do appraisals but offered to do a free market analysis, which he happily accepted. He may call me about listing it later on, but that’s not the point. I’m happy to be of service.

I follow a policy that I came to embody many years ago: Concentrate on giving and the getting will take care of itself.

If the General Assembly follows the recommendation of DORA’s “sunrise” report, we may see the return of regulation of HOA management companies and of the community association managers (CAMs) they employ.

DORA’s recommendation, released earlier this month, stated that regulation of CAMs “is necessary to protect consumers” and recommended the creation of a new regulatory program.

CAMs were regulated starting in 2015, but the bill to retain that regulation (which DORA recommended) was killed by the General Assembly in 2017 resulting in the phase out of CAM regulation in June 2019. With the General Assembly now controlled by Democrats, this new recommendation may result in legislation restoring regulation of CAMs that will be signed into law by Gov. Polis.

You can find the full text of DORA’s sunrise report here.

You can’t tell a book by its cover, and you can’t tell a home’s condition by how well it looks when you fall in love with it and go under contract.

That’s why you should never waive your right to inspect the home and submit an “Inspection Objection.” With all the bidding wars going on, it’s increasingly common for buyers to waive both inspection and appraisal in order to get the home they are bidding on.

There are three inspection deadlines. You might feel the need when competing with other buyers to waive inspection objection and inspection resolution, but you should never waive inspection termination. That way, you still have the right to hire a professional inspector, and you may just find enough hidden defects to exercise your right to terminate the contract.

That’s what happened with a buyer I was working with. The house showed all the signs of being well built and well maintained, but the inspection revealed several shocking structural flaws, electrical issues and plumbing problems. We clearly had to terminate — unless the seller was willing to amend the contract to allow for inspection objection and inspection resolution, which she did. (Lesson: The threat to terminate alway contains within it the possibility of restoring the right to submit an inspection objection which you may have given up to win the bidding war.)

We then submitted an extensive list of repairs, which the seller rejected completely. This was unusual, however, since the seller and her agent were now aware of serious problems, structural and otherwise, which they were required by law to disclose to the next buyer.

Roughly 6.5 million homebuyers have taken advantage of ridiculously low interest rates since the beginning of 2021. Low interest rates have allowed them to become first-time homebuyers, to move up to their dream home or to downsize.

Many would-be home purchasers have watched this ‘boom’ from the sidelines and decided that now may not be the best time to buy. Bidding wars and the need to make split second buying decisions over the last few months have reduced their appetite for home buying. It might be time to reconsider that decision.

I asked Jaxzann Riggs about the wisdom of “waiting” to make a move, and the following is based on our conversation.

Rental rates fell in 2020, but nothing could be further from the truth in 2021. While accounts vary, some leasing agents (according to ApartmentList.com) report that rental rates could increase as much as 32.4% in the next 12 months and stats indicate that they are up a shocking 16.5% in the first eight months of 2021.

As rental prices spike, potential homeowners should do a little mortgage math.

A potential homeowner who is paying $2,600 per month for rent, would be able to own a home valued at around $475,000. With a 3% down payment of around $14,279, this renter could turn into a homeowner, allowing them to enjoy the associated tax benefits and the opportunity for appreciation on their new property

Housing inventory is increasing and with the threat posed by rising rental rates, and rising interest rates, there is no better time than today to explore home buying options.

During the Covid-19 pandemic, the Federal Reserve supported lending to households, consumers, and small businesses to stimulate the economy. The Federal Reserve recently signaled that it plans to begin reducing the support it has been providing to the U.S. economy. Long term fixed mortgage rates are driven by the overall economy and inflation, but they are directly influenced by Fed policy.

Once the Federal Reserve starts to slow the pace of bond purchases, mortgage rates willmove up. Fed officials indicated that they would begin “tapering” the asset-buying activities that it began last year as early as November. After the announcement, mortgage rates did in fact, show a rising trend. For someone with a $500,000 home loan, a 4-basis point jump will cost them $115 more per month and $41,400.44 more over the life of the loan on a 30-year, fixed-rate mortgage.

Mortgage rates are hovering near 3% and demand remains strong but higher rates are clearly on the horizon. Remember our potential renter? As rates rise, a monthly rent of $2,600 would instead result in a $410,000 house (vs. $475,000), if interest rates move from 3% to 4.5%

Even more incentive to potential homeowners is housing inventory. The inventory of active listings on the market rose by a record monthly amount (according to Denver Metro Association of Realtors). Some potential homebuyers that I am working with report they are waiting for prices to cool off to make offers, but even if that does occur, they are unlikely to see lower monthly house payments because any potential savings in purchase price will be lost to rising interest rates.

Future home buyers are not the only ones affected by higher interest rates. For homeowners who have been procrastinating with their refinance application, now is the time to call a lender. Jaxzann Riggs and I are standing by to make the process as simple as possible.”

If you have lending questions, you can reach Jaxzann, who is the owner of The Mortgage Network, at (303) 990-2992.

The often heard complaint from homebuyers and their agents during the pandemic was the lack of active listings, which was not due to a lack of new listings but rather the result of those new listings going under contract so quickly that at any given time there were few to choose from.

It became a crazy sellers market which is only now abating except for “special” homes that are priced appropriately.

Looking only at closed listings, you might conclude that we are still in a sellers market. One measure I have used in the past is the median ratio of listing price to closing price, which remains above 100% within the Denver metro area. In September, for closings within 15 miles of downtown Denver, the median was 0.9% above listing price — declining, but still impressive.

However, if you look below the surface — that is, at the homes that haven’t sold, you see a rising inventory of homes that have been active on the MLS for an increasing length of time.

For example, as I write this column on Monday morning for this Thursday’s newspapers, there are 2,542 active listings of single family homes, condos and townhomes within 18 miles of downtown Denver, 760 of which (or 30%) were only listed on REcolorado in the last 7 days.

Despite so many new listings, the median active listing has been on the MLS for 19 days, and 1,024 of them (or 49.9%) have been active 30 days or longer. Another 552 of them (or 21.7%) have been active for 60 days or longer.

Meanwhile, there are 4,949 pending listings within that same 18-mile radius. Of them, only 804 or 16.2% were active more than 30 days before going under contract, and only 319 (or 6.4%) took over 60 days to go under contract. 221 of those currently pending listings went under contract with zero days on the MLS. Another 2,528 of them (over 50%) went under contract in 1 to 7 days.

Meanwhile, if you look at the 3,509 listings in the same 18-mile radius that closed in the last 30 days, only 401 of them (or 11.4%) took over 30 days to go under contract, and only 318 (or 3.4%) took over 60 days to go under contract.

This is what it looks like as we transition from a seller’s market to a balanced market. To reiterate, nearly 22%of active listings within 18 miles of downtown Denver have been on the market over 60 days, but only 3.4% of recently closed listings were active that long before going on the market.

My bottom-line observation is: Buyers who gave up after losing multiple bidding wars will find greater success if they re-enter the market now. As I’ve suggested in the past, you can avoid a bidding war simply by asking your agent to send only listings that have been active on the MLS for at least 10 days. You’re less likely to have competing buyers for them.

The new listings, however, will still get multiple offers if they are unique or special in one way or another.

For example, we recently listed a home in Golden’s coveted 12th Street Historic District. There was a bidding war on it, and it went under contract for more than $100,000 over the listing price. But if you look at all the active listings in Golden proper as I write this, there is only one new listing. The other active listings have been on the MLS between 11 and 102 days, and all but two of them have posted price reductions.

It should begin to sink in among sellers and their listing agents that they need to be less aggressive in pricing their homes when they put them on the market.

Don’t assume that buyers will flock to your listing regardless of price and compete with each other for it. Price it right, and it will sell. Overprice it, and it won’t.

The real estate industry runs on electronic signatures nowadays. In our market most contracts are created and signed on CTM eContracts. Buyers and sellers can click on “Select Font Signature” and see their name appear in a script font. Then they click “Save” and click “Accept” to show that they accept that the font signature is theirs. That document is considered signed.

In the beginning, I was leery of this technology, insisting that our clients use a stylus or finger to personally sign their name on a touch screen device such as a smartphone. Ultimately I relented, realizing that the closing based on those electronically signed documents does involve a “wet signature” witnessed by a Notary.

Electronic signatures became legal as a result of UETA, the Uniform Electronic Transactions Act,which became law in 1999. It was followed in 2000 by the E-Sign Act, which legalized electronic signatures for interstate and international transactions. The following is from www.BakerMckenzie.com:

UETA provides a framework for states to enact state law concerning the enforceability of e-signatures and the validity of electronic records. Forty-seven states and the District of Columbia, Puerto Rico and the US Virgin Islands have adopted some form of UETA. The only states that have not adopted UETA are New York, Illinois and Washington, but each of these states has enacted legislation similar to UETA to govern how electronic transactions are handled….

UETA and the E-Sign Act provide that: (a) a record or signature may not be denied legal effect or enforceability solely because it is in electronic form; (b) a contract may not be denied legal effect or enforceability solely because an electronic record was used in its formation; (c) if a law requires a record to be in writing, an electronic record satisfies the law; and (d) if a law requires a signature, an electronic signature satisfies the law.

It followed, as a result of this law, that electronic messages (emails) between two parties can constitute a contract if both parties have signed their emails by typing their names. The more detailed the emails (covering terms as well as price) the more likely that a court would deem them enforceable contracts.

A Sept. 28 article on Forbes.com by Joshua Stein carried the headline, Yes, Sending an Email Can Create a Binding Contract. It reported on an appellate court decision in New York State that went further to declare that typing your name on such emails was not necessary, that merely clicking “send” from your email account made any signature “an unnecessary formality.” Here are some key paragraphs from that Forbes article:

This case means that pressing “send” on an email is now potentially equivalent to signing a piece of paper containing whatever statements appeared in the email. An actual typed signature is not necessary….

The moral of the story: before sending an email that could be interpreted as committing to some agreement, consider whether that’s what you really want. If not, make it clear in writing that your email isn’t intended to create any form of binding agreement.

Many standard email disclaimers say exactly that, automatically, on every message that goes out. Careful email senders should not rely on those disclaimers to protect them. If an email sounds like a serious and meaningful agreement to material terms, the courts just might decide that’s what it is, and enforce it accordingly.

Although that was the decision of a New York State appellate court, we should probably consider that Colorado courts or the United States Supreme Court might issue a similar opinion. So, how does this affect buyers and sellers of real estate?

If you’re represented by a real estate agent, you’re not sending emails directly to the other party in a transaction, but if you are unrepresented and you exchange emails with a prospective buyer or investor, you could easily find yourself negotiating and agreeing to terms and price before undertaking the creation of a contract with various other important terms and deadlines. Be careful!

At the very least, when discussing price and terms with a prospective buyer or seller, always add that “this is not a contract, which still needs to be created separately and signed by both parties.”