The practice of including “love letters” or personal letters with home offers has been a common practice in real estate transactions. These letters are intended to convey the emotional connection and personal story of the buyer to the seller, potentially appealing to their sentiments and influencing their decision.

However, it’s important to note that the acceptability and effectiveness of love letters can vary based on local regulations, cultural norms, and individual seller preferences. Additionally, there are legal considerations surrounding fair housing laws, which aim to prevent discrimination in the housing market.

In some regions, love letters are discouraged or even prohibited to avoid potential bias or discrimination in the selection process. These laws are in place to ensure fair treatment and equal opportunities for all potential buyers. If love letters are permitted in your area, here are some factors to consider:

Pros:

1. Emotional Appeal: A heartfelt letter can establish a personal connection and create empathy between the buyer and seller. It may help the seller relate to the buyer’s story and motivate them to choose an offer.

2. Differentiation: In competitive markets, where multiple offers are common, a well-crafted love letter can make your offer stand out from the rest. It allows you to differentiate yourself by showing your genuine interest in the property and willingness to create a home.

Cons:

1. Fair Housing Concerns: Love letters have the potential to inadvertently disclose personal information that could trigger bias or discrimination. Sellers may unintentionally make decisions based on protected characteristics such as race, religion, or family status, which is a violation of fair housing laws.

2. Unintended Pressure: Sellers might feel pressured or uncomfortable when evaluating offers accompanied by emotional letters. They may prefer to base their decision solely on objective factors such as price, terms, and reliability of the buyer.

Given the complexity of this topic and the varying legal and cultural considerations, it is advisable to consult with a local real estate professional or attorney who can provide guidance specific to your location. They will be familiar with the local regulations and can help you navigate the decision of whether or not to include a love letter with your offer.

—End of article written by ChatGPT

If I had written on this topic, I would have provided more guidance on avoiding fair housing violations, which is what triggered Oregon’s 2022 law banning love letters. That law was found unconstitutional on May 6th. I would have advised to exclude any photograph of the buyers. Let’s say the picture was of a white couple, and their offer was accepted over an offer from at least one gay or mixed race couple. That losing buyer might well win a lawsuit claiming that the seller and listing agent committed a fair housing violation, if they were to discover the winning love letter.

Fair housing laws, both at the federal level and the stricter Colorado state level, include so many “protected classes,” that a seller is not allowed to consider even the familial status (married, single, with or without children), disability, or sexual orientation, including transgender status, along with the more familiar race, creed, national origin, etc. As you can imagine, it would be hard to compose a “love letter” that didn’t reveal at least one of those descriptors.

In November 2019 the National Association of Realtors (NAR) created its Clear Cooperation Policy (CCP) designed to end the practice of “pocket listings.” A pocket listing is one which an agent keeps in his or her “pocket,” hoping to sell it himself instead of giving other agents the opportunity to sell it. The incentive is financial. Roughly half the listing commission goes to the agent who sells a listing. If an agent sells the listing himself, he/she gets to keep the entire commission.

The term “clear cooperation” is a reference to the purpose of the MLS, which is “cooperation and compensation.” Every MLS member agrees to cooperate with other MLS members, allowing them to sell their listing. And every listing specifies the compensation which the buyer’s agent will receive — typically 2.5 to 2.8 percent in our market.

You can read the three previous articles I’ve written about this policy at www.JimSmithColumns.com. Those articles (in Nov. 2019, Feb. 2021, and Aug. 2021) document the creation of the CCP and its subsequent implementation by REcolorado, our MLS. The deadline set by NAR to do so was May 1, 2020.

My August 12, 2021, column described how our MLS is fining agents $1,500 for a first offense when they fail to put a listing on the MLS within one business day of promoting it outside their own office in any way — online, in print or via a sign in the ground.

One would think that with such a big penalty the number of homes selling with zero days on the MLS would have declined, but in fact they have increased. I didn’t realize that until I read a Nov. 3rd article from Inman.com which quoted a study by Broker Resource Network (BRN). The study pulled data from 24 multiple listing services comparing the number of homes sold with zero days on MLS during the 12 months before and after the May 1, 2020, implementation date.

“In every market reviewed across the United States, brokerages recognized double and triple digit increases in Zero Days On Market listings across firms of all sizes and business models,” the report said. These were figures for big brokerages, not the full MLS.

So I checked REcolorado statistics to see what our full-MLS statistics are for homes sold with zero days on the MLS. I found that there were 2,225 such closings reported in the 12 months before May 1, 2020, and 2,769 reported in the 12 months after May 1, 2020 — a 24.4% increase.

To discover the longer trendline, I looked at several half-year periods going back to 2018. In the last 180 days (as of this past Sunday), there were 1,677 closings of resale residential listings recorded on REcolorado with zero days on MLS before going under contract.

During the same 180 days of 2020, there were 1,295 such closings, making this year a 29.5% increase over last year. The number in 2019 was even lower — 1,077. In 2018 it was not much different — 1,104.

What could account for this counter-intuitive increase?

One explanation might be the explosion of the seller’s market during the pandemic, which really took off simultaneously with the implementation of the Clear Cooperation Policy (and the pandemic surge).

One way to assess the seller’s market is to measure how many homes went under contract after 4 days on the MLS during those 12 months before and after May 1, 2020, and the median ratio of sold price to listing price for those listings.

During the 12 months before the implementation of the CCP, there were 4,563 closings of listings which went under contract in 4 days, and the median ratio of sold price to listing price was 1.0019. During the 8 months after May 1, 2020, there were 4,896 such closings, and the median ratio was 1.01299. Another 2,840 such closings took place during the remaining 4 months of the 12-month period after May 1, 2020, and the median ratio for them was 1.05157. Clearly, the seller’s market was accelerating. It makes sense that more sellers might receive offers they “can’t refuse,” and that listing agents might encourage them to accept those offers.

There was an important loophole created when the CCP was implemented by REcolorado and perhaps by those 24 other MLSs. That loophole is called the “office exclusive,” which allows any brokerage to promote an off-MLS listing within the brokerage, so long as there is no advertising of any kind on social media or in print and no sign in the yard — the definition of a pocket listing.

This policy greatly favored large brokerages which could have hundreds of agents in a dozen or more offices, to promote new listings internally with the additional incentive of keeping the full commission of each transaction within the brokerage.

If this loophole were to be closed, there would probably be far fewer closings with zero days in the MLS — and sellers might get more money for their homes by having them exposed to more competing buyers.

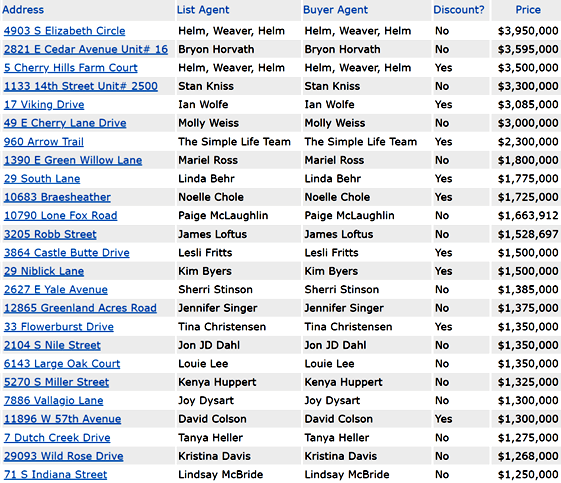

As I mentioned above, a listing agent profits from keeping a listing off the MLS, because it increases the chances of selling the listing himself and thereby greatly increasing his/her commission. Of the 100 homes on REcolorado which sold for $1.25 million or more in the last 180 days with zero days on the MLS, 25% of them were double ended (see list below), and only 9 of those 25 listings reduced the commission paid by the seller because of their listing agent’s windfall. (The agents at Golden Real Estate always discount our commission when we double-end a transaction.)

D0uble-Ended Sales On REcolorado Over $1.25 Million – Last 180 Days, Showing Whether Seller Got a Discounted Commission

By contrast, of the 100 highest priced homes ($1,575,000 and over) which sold after 4 days on the market, only 2% were double-ended. Whether or not you call it “greed,” the agents who kept their homes off the MLS greatly profited from it — and the sellers paid the price by not exposing their homes to all potential buyers.

Another recent article from Inman reminds us that Fair Housing was one of the reasons the Clear Cooperation Policy was introduced. A blog post on REcolorado also makes this point. The reasoning is that if a home is sold privately without being exposed to all buyers on an MLS, then it is more likely to be sold within the same demographic. Thus, pocket listings are inherently discriminatory against minority groups, whether they be racial or, for example, LGBTQ.

I’m sure that these articles and the studies behind them, including my own analysis of REcolorado statistics herein, will lead to some discussion locally and nationally about how to tweak the Clear Cooperation Policy so it is more effective and less counter-productive, which it clearly has proven to be. I do not believe, however, that the Clear Cooperation Policy will be scrapped, because its stated intention is clearly good public policy.

Sellers: Insist that your home is put on the MLS so that all interested buyers have the opportunity to see it and participate in a bidding war that nets you more money.

Until recently it was a common practice for buyers’ agents to submit a “love letter” with their offers, hoping to convince the seller to choose their buyer over others in a bidding war.

That practice has fallen out of favor, however, as doing so might constitute a violation of federal Fair Housing rules as well as of the Realtor Code of Ethics.

Article 10 of the Code includes the following: “Realtors shall not be parties to any plan or agreement to discriminate against a person or persons on the basis of race, color, religion, sex, handicap, familial status, national origin, sexual orientation, or gender identity.” Such discrimination is also a state and federal fair housing crime.

It would be hard not to reveal any of the above characteristics in a “love letter,” especially if it contains a photo of the buyer or buyer’s family. But there are other subtleties to consider. One of the sessions at last month’s National Association of Realtors conference was titled, “How to Stay Out of Trouble: Risk Management and the Code of Ethics,” taught by Barbara Betts, a California Realtor who is also a hearing officer for violations of the Code of Ethics.

In her talk, as reported by Inman News, Betts described how risky such letters could be, especially for the seller and listing agent. “Sellers are humans. Even though they are not purposely trying to create a fair housing situation for themselves, they inadvertently are,” she said. “When the seller gets these letters, they get excited to sell the home to someone they feel will fit into their neighborhood, and that’s where there’s a problem.”

The danger is intensified when there are competing love letters. Imagine, for example, that one of the buyers reveals himself to be a single African American who says your home is perfect for him because he is wheelchair-bound, but your seller chose a family with children who liked your home because it’s close to their synagogue. That choice has offered a veritable smorgasbord of fair housing violations that the rejected buyer could mention in a fair housing complaint, and that their broker could cite in a Code of Ethics complaint against the listing agent.

“We need to consider raising fair housing concerns with our buyers,” Betts advises her fellow Realtors. “Don’t read or accept these letters that are drafted by a buyer. Certainly do not give any support or suggestions. As listing agents, we definitely need to discuss the potential liability during the listing interview and not deliver or accept these letters for the seller.”

Betts added, “If the letter is all about ‘I love your home. It’s beautiful. I love how you’ve remodeled it, I promise I won’t tear it down and remodel it,’ there aren’t any fair housing violations in those statements. The second you start talking about family, color, race, religion, marital status, those things instantly become possible fair housing violations.”

For all these reasons, the agents at Golden Real Estate no longer submit or accept “love letters” from buyers. If we receive one, it’s best that we don’t even read it and that we inform the buyer’s agent that we have deleted it.

There are other ways in which Realtors can commit a fair housing violation, perhaps unconsciously. One is the practice known as “steering,” in which an agent recommends different neighborhoods to different buyers based on where they would “fit in” because of their race, color or religion. We must truly be blind to such characteristics and give the same information to all buyers. Fortunately, buyers do their own searching most of the time. As agents, we must show any buyer what they want to see without comment of any kind.

When a buyer from out of town asks us to describe our neighborhoods, it’s best to avoid all demographic descriptions, limiting ourselves to describing the housing stock, price range, etc. We must not provide such information with an intention to steer them based on their profile.

Meanwhile, sellers expect us to show their homes only to qualified buyers, but if we ask some buyers but not others to be pre-qualified by a trusted lender before showing a listing, we open ourselves to possible fair housing complaints.

We’d all like to believe that racism and other kinds of systemic or cultural discrimination are artifacts of the past, but we are more aware than ever that such discrimination exists even within ourselves, hopefully unconsciously. Unconscious or not, we need to realize that beyond being morally wrong, it can get us into serious professional trouble as agents and that it can also put our clients at risk, making it more important than ever that we educate our clients about the risks they could be facing.

On his first day as president of the National Association of Realtors, Charlie Oppler said NAR will continue to advocate for equality and inclusion in real estate, and he apologized for NAR policies in the 1900s that contributed to discrimination and racial inequality.

Oppler spoke during the Diversity and Inclusion Summit, issuing a sobering message that sets the tone for his priorities as president of the 1.4-million member organization. “What Realtors did was an outrage to our morals and our ideals.” said Oppler. “It was a betrayal of our commitment to fairness and equality. I’m here today, as the president of the National Association of Realtors, to say we were wrong.”

“We can’t go back to fix the mistakes of the past,” Oppler continued. “But we can look at this problem squarely in the eye. And we can finally say, on behalf of our industry, that what Realtors did was shameful, and we are sorry.”

Oppler recognized the fact that “words aren’t enough,” emphasizing that the association and all Realtors should take “positive action to remedy decades’ worth of inequality.”

We at Golden Real Estate applaud Oppler for his strong statement on this subject.

As you’d expect from any Democratic administration, there will be an increased focus on middle class and low income communities’ needs in the Biden administration, and that includes housing policy.

Back in February, after losing the Iowa caucuses and the New Hampshire primary, and prior to the South Carolina primary, Biden released a $640 billion housing plan, focused primarily on increasing home ownership among Americans. Among other things, it included a $15,000 tax credit for first-time home buyers that could be used as part of the down payment at time of purchase.

“People vote based on their pocketbooks, and you don’t get a bigger pocketbook issue than housing,” realtor.com’s chief economist Danielle Hale said. “For many, [housing] is the largest monthly expense that they have. And if you own a home, it’s likely the most valuable thing that you own.”

According to Clare Trapasso’s article on realtor.com, Biden’s plan also includes down payment assistance for teachers and first responders plus changes in the appraisal process to address racial disparities. The down payment assistance, however, would be conditioned on purchasing in targeted low-income areas in need of investment.

It has long been understood that home ownership is central to building family wealth, supported statistically by the Federal Reserve’s Survey of Consumer Finances. The report covering the period 2013-2016 showed that during that period the median net worth of homeowners rose by 15% to $231,400, while the median net worth of renters fell by 5% to only $5,200. In other words, as of 2016, homeowners’ median net worth was 44.5 times that of renters.

A new 3-year survey covering the period 2016 to 2019 was released in September.

As you’d expect, there’s a racial component to the homeownership divide. According to Svenja Gudell, chief economist of Zillow Group, nearly 75% of white households own their own home, while less than half of black and Hispanic households are homeowners.

Although redlining of low-income communities, which was promoted by the FHA from its inception in 1934, was outlawed by the 1968 Fair Housing Act, the damage had been done, and it will be hard for any administration to undo it. We are just beginning to understand the problem and how to solve it.

The Biden plan also includes increased funding of Section 8 vouchers for low-income renters. At present, there’s only enough Section 8 funding to meet 25% of the demand. The plan would also prohibit landlords from discriminating against prospective tenants using Section 8 vouchers, and would provide legal assistance to tenants facing eviction.

The most progressive element of Biden’s plan may be his proposal to provide a tax credit so that no renter pays more than 30% of his/her income toward rent, estimated to cost $5 billion/year.

The plan speaks about appraisal reform, aiming to create a national standard to assure that homes in minority communities are appraised for the same as homes in comparable white communities, but that defies the core principle of appraisal — that a home is worth what a willing arms-length buyer will pay for it.

According to the realtor.com article, the Biden plan promotes the creation of a public credit agency that would take into consideration a positive history of payment of rent and utility bills, providing a higher credit score that could help renters qualify for a home mortgage.

Not mentioned in the realtor.com article about Biden’s housing plan is the president-elect’s promise to undo the elements of Trump’s tax law which favored the wealthy. However, one provision actually harmed the wealthy who live in states with high property taxes, many of which, coincidentally, voted for Hilary Clinton.

That was the provision regarding SALT — State and Local Taxes, composed primarily of real estate taxes and income tax. It limited the deduction of those taxes to $10,000 per year. I suspect that this element of the tax code will be changed under the Biden administration.

The Trump tax law also doubled the standard deduction to $24,000, which eliminated for many the benefit of charitable donations. I, for one, thought this would spell doom for many non-profit organizations, although Giving USA re-ports that donations by individuals fell only 3.4% in 2018. That’s remarkable, given that the number of taxpayers who itemized deductions fell that year to 18 million, from 46.5 million the year before, according to the Joint Committee on Taxation (per accountingtoday.com).

Those of us who are into sustainability and fighting climate change can expect the new administration to incentivize energy efficiency improvements and building codes through tax credits and grants. When Trump took office, there was a lot of concern in Golden and Jeffco that the Department of Energy, whose secretary had advocated abolishing the department until he learned it was responsible for America’s nuclear arsenal, would defund the National Renewable Energy Laboratory, but funding was actually increased by Congress. We can expect that a Biden administration will provide even greater funding to NREL, energy efficiency, sustainability and the electrification of transportation.

Biden’s February housing plan does address this issue, with the goal of cutting the carbon footprint of buildings by 50% by 2035, and providing incentives to home owners who retrofit their homes to be more energy efficient and more solar powered.

While it might be popular to think of Realtors as privileged conservatives (mostly Republicans) who put up with but are not fans of federal civil rights laws, quite the opposite appears to be true now. Liberal thinking Realtors are in ascendance.

An August 22 article from Realtor Magazine, the official magazine of the National Association of Realtors, makes this abundantly clear.

The Chicago Association of Realtors, headed by an African-American woman, apologized last year for its “historically racist policies that persisted for decades.”

Click on that link above. Unless you miss the “good old days,” you’ll be heartened by what you read. It makes me proud to be a Realtor. The commitment to equality and justice is rock solid.

From my first classes in real estate, back in 2002, I was made aware of our obligation under law as well as under the Realtor Code of Ethics, to avoid even the hint of racial and other discrimination, including “steering” buyers to or from neighborhoods based on race or other criteria.

We continue to be warned about “testers” from the U.S. Department of Housing & Urban Development who pose as buyers to see whether we are in fact engaging in steering or other discriminatory practices.

I am reminded of this topic by an article in the current issue of Realtor Magazine about “The Gentrification Conversation.” You are probably familiar with this term, which refers to the upscaling of traditionally poor and usually minority neighborhoods, resulting in the displacement of minority homeowners and tenants as they are priced out of their long-time neighborhoods.

While we don’t see a lot of gentrification in our suburban counties, it has been and remains an issue in inner cities such as Denver, and I see it a lot in West Denver, between Sheridan Blvd and I-25.

The Realtor Magazine article talked about the large-scale gentrification taking place in Detroit and about the deployment of HUD testers:

“An investigation by Newsday [a Long Island daily newspaper] published in November found disparate treatment and evidence of fair housing violations when undercover testers posing as home buyers visited real estate agents throughout Long Island, N.Y. A total of 93 agents were tested over three years, and the probe found unequal treatment occurred 49% of the time with black testers, 39% with Hispanic testers, and 19% with Asian testers. Unequal treatment included showing minority testers fewer properties, steering testers toward certain neighborhoods, and refusing to serve minority testers who weren’t preapproved for financing but not requiring the same for white testers. Agents also used euphemisms to communicate the racial makeup of an area and imply racial bias.

“[National Association of Realtors] President Vince Malta says he was deeply troubled by Newsday’s findings…. ‘NAR maintains its strong support of fair housing testing to unmask housing discrimination and hold our industry to the highest standard,’ he says.”

It should be noted that race is only one of several “protected classes” under both state and federal laws. The federal Fair Housing Act of 1968 also prohibits discrimination based on sex, color, religion or creed, national origin and disability. Colorado law goes further, prohibiting discrimination based on sexual orientation (including transgender), gender identity, and familial status (single, married, having children under 18, being pregnant, etc.).

Avoiding fair housing violations can be tricky. Did you know that hoarding and peanut allergies are classified as disabilities? Or that age discrimination is not prohibited in Colorado? Or that drug addiction is protected as a disability, but illegal drug activity isn’t? Or that you can’t discriminate based on how a person earns their income? Or that you can be held liable for violating the Fair Housing Act even if you did not intend to discriminate?

The Realtor Magazine article provides guidance on how to avoid committing a fair housing violation. For example, we cannot answer questions about a neighborhood’s demographics, but we can provide a neighborhood report from Realtor Property Resource (RPR) which does provide such information. We cannot characterize a neighborhood’s level of crime, but must refer the buyer to the local police department.

We can avoid “steering” by entering the buyer’s search criteria into the MLS and letting the computer pull all listings matching those search criteria. We can enter geographical criteria such as city or draw an area on a map, as long as we are following the buyer’s request and are not knowingly avoiding one area or another based on discriminatory preferences.

If a buyer asks us to help them identify areas based on discriminatory criteria, we are advised to decline to serve that buyer. Since I have never had a buyer make such a request, I would suspect such a buyer to be a HUD tester.

The trickiest conversation to navigate would be one asking about the trends in a given neighborhood. Is it “going up” or “going down”? All we should do is provide actual statistics about the past few years, just giving the numbers, but no interpretation of them that could include demographic changes.

I can’t recall dealing with a buyer who presented a fair housing challenge, and I make an effort to stay aware of fair housing laws and understand the importance of non-discrimination. However, it can be a challenge keeping up with current housing laws, as suggested by those questions I posed above.