Perhaps you heard that the House of Representatives passed and sent to the Senate a bill making the District of Columbia the 51st State. It will die in the Republican-controlled Senate.

The United States is likely the only country in the developed world where residents of its capital city have no voting representation in their government. It was only 60 years ago that D.C. was given 3 votes in the Electoral College, and it still has no voting representation in Congress. Republicans will never accept that because the District is overwhelming Democratic. (Trump got 4% of the vote in 2016.) In 2000, the District added the phrase “Taxation Without Representation” to its license plates, and newly elected President George W. Bush responded by ordering that US Government plates replace the D.C. plates on all White House vehicles. Since then, the verb “End” was added to the controversial phrase.

As a compromise, I suggest that the residential areas of D.C. be annexed into Maryland, giving that state another seat or two (based on population) in the House of Representatives. Perhaps Republicans could accept this approach since it wouldn’t produce two Democratic U.S. Senators, just one or two Democratic representatives.

With the new reckoning about systemic racism in America, the Houston Association of Realtors (HAR) decided that “master bedroom” should be replaced with “primary bedroom,” according to a CNN report.

So long as guest bedrooms aren’t called “slave bedrooms,” I see nothing wrong with the term “master bedroom.” (And what slaveowner ever had his enslaved workers sleeping in adjoining bedrooms under the same roof?)

I checked with REcolorado, our local MLS (which is separate from but owned by our local Realtor associations), and I was assured that there is no plan here to follow HAR’s initiative, and I suspect frankly that HAR will have second thoughts about that change. I agree with John Legend, whose response was to ridicule the change and tell them to concentrate instead on the very real issue of discrimination in real estate.

That’s what it’s like for Jim & Patty Horan, who bought their 3-bedroom, 3-bath, 2,135-sq.-ft. home at 15062 W. 69th Place in Arvada’s Geos Community. They paid $525,000 for it three years ago (July 2017).

Like all Geos homes, this one has no gas service. With only 6kW of solar panels on the roof, the home is heated by a ground source heat pump. It draws heat from the earth via a 300-foot-deep loop under the home. The heat pump uses very little electricity during the summer to further cool the 55° fluid in that loop, and not much more energy during heating season to heat that fluid to 100 degrees.

On Saturday, June 27th, Jim Horan gave me a tour of his home which I recorded for this fall’s Metro Denver Green Homes Tour. You can view the video at YouTube.com/jimsmith145.

Geos Community’s website describes it as “Colorado’s first geosolar development” and is the only subdivision I know that’s built entirely “net zero energy.” There are developers building solar-powered communities like KB Home’s subdivision on the northeast corner of Hwy 93 and 58th Ave., but they don’t come close to being net zero.

There’s a term for such homes — “greenwashing,” which Wikipedia defines at “a form of marketing spin in which green PR and green marketing are deceptively used to persuade the public that an organization’s products, aims and policies are environmentally friendly.” I’ve always marveled that those KB Homes were built with many of the solar panels installed on north-facing roof surfaces.

Getting back to the Horans’ home, there’s more to going net zero than having solar panels and a ground-source heat pump. Those features must be coupled with energy saving features so that the limited number of solar panels are enough to meet the home’s energy needs — with energy left over to charge an electric car.

Here are some of those features which I covered in my video tour with Jim Horan.

First and foremost is the passive solar orientation of the building with lots of south-facing windows and a south-facing roof for solar panels. Also, there are overhangs above each south-facing window designed to shade it from the sun during the summer while allow full sun in the winter when the sun is lower in the southern sky.

Next, the building’s “envelope” has to be very tight. That starts with foam insulation blown onto the interior surfaces of the roof and exterior walls, replacing the blown-in cellulose and fiberglass batting typical of tract homes built by other developers. The windows are Alpen triple-pane windows which also have foam-insulated fiberglass framing. (Fiberglass is better for window framing than vinyl – not as prone to aging and warping.)

Those elements make a house too air-tight for healthy living, so an energy recovery ventilator is installed which constantly brings in fresh air, using a heat exchanger designed so that the heat (or coolness) of the air being exhausted is used to heat or cool the fresh air being brought into the house. A heat pump within this device, called a CERV, provides further heating or cooling of that fresh air as needed.

In the townhomes at the Geos Community, the CERV works with an air-source heat pump mini-split instead of a ground-source heat pump to heat and cool the home year-round.

Have you heard the term “indoor air quality” or “sick building syndrome”? It refers to high levels of CO2 or volatile organic compounds (VOCs) which can build up in a home, especially in a home as air-tight as the Geos homes.

The CERV monitors both CO2 and VOC levels in the house and will bring in additional fresh air when those gases exceed the level set by the homeowner. (The Horans have the level for each gas set at 950 parts per million, or ppm.)

What are VOCs? If you can smell it, it’s probably a volatile organic compound. Examples include new carpet smell and, worst of all, cat litter smells.

Two appliances in Geos homes also contribute to their low energy load. One is the Bosch condensation clothes dryer, which pulls in cool, dry air from the room. The air is heated and passed through the clothes; but instead of being vented outdoors, the air travels through a stainless steel cooling device or heat exchanger. It does heat the room it is in, so the Horans choose to dry their clothes on an outdoor line during the summer, even though their heat pump could handle the additional cooling load if they didn’t do that. Home Depot sells the Bosch 300 “ventless” dryer for $989.

The other appliance is the heat-pump water heater. It has a heat pump above the tank which transfers the heat from the room into the water. I’ve written about this product before. Home Depot sells a 50-gallon Rheem model for $1,299which earns a $400 rebate from Xcel Energy and another $300 in federal tax credit if purchased by December 31, 2020. Because this appliance emits cold air, it’s in a pantry which the Horans keep closed in the winter and open in the summer. (I would put it in a wine cellar or in a room with a freezer, which emits hot air — a symbiotic arrangement within one room.)

As you are beginning to gather, building a net zero energy home is best done from scratch, when the additional cost is less than retrofitting a home. (My home is net zero in terms of electricity, but we still burn $30 to $50 of natural gas each month, and it takes twice as many solar panels for my home, which has about the same square footage as the Horans’.)

You may be wondering how much more it cost to build the Horans’ house, which they bought new in July 2017. To answer that, I searched all the comparable homes (2– or 3-story, between 1,500 and 2,500 square feet within 1 mile radius) sold during the summer months of 2017, and I found that the $246 per finished square foot paid by the Horans was actually below the median price ($253 per finished square foot) for the seven comparable sales. And those homes probably pay thousands of dollars per year more for electricity (and gas) than the Horans.

If you want to learn more about Geos community, give me a call at 303-525-1851 or visit the Geos website, www.DiscoverGeos.com.

In this era of “Big Data,” there are companies which specialize in providing hungry real estate agents with the names and addresses of homeowners with high “sell scores.”

You can tell if you have a high sell score by how many solicitations you have received by letter, postcard, phone call, text message or email about selling your home.

If you bought your house in the last year or two, you have a low sell score and probably aren’t getting such solicitations, but if you’ve lived in your house a long time and are of a “certain age” that suggests you are an empty nester, you probably get a lot of solicitations, especially from investors, but also from real estate agents who purchase lists with your name, address and phone number.

And these parties don’t pay much attention to Do Not Call lists.

Licensed real estate agents can subscribe to an app called Forewarn which allows us to get your phone numbers, including cell numbers, just by entering your name and ZIP code. I have this app myself. It’s marketed to us as a safety tool to forewarn us about buyers with criminal records, judgments or liens, etc. Armed with that information, we can decline requests to show listings either because they’re not qualified financially or we suspect they might rob or assault us. To get such details on the app, we enter the phone number which appeared on Caller ID, or we search by name and city or ZIP code, if we know it.

In prospecting, it’s a “numbers game.” It only takes a small percentage of persons to “bite” to make the practice of over-soliciting everyone else worth the time and expense, so there’s little you can do to stop it. However, here’s some practical advice on reducing those solicitations by just a little.

Regarding text messages, replying with “Stop” should at least reduce follow-up texts, and if it’s a robo-text, the computer will probably reply instantly with “You’ve been unsubscribed.” That is my favorite text message to receive!

If it’s a phone solicitation, you can block the number on most cell phones. On my iPhone, after I hang up, I find the number under “Recents” and click on the circled “i” at the right, scroll down and click on “Block this Caller.”

Many email programs also allow you to label an email as “junk” and to block that email address. In Outlook (which I use), the “Junk” designation is at the very left of the “ribbon” at the top of my screen, to the left of the “Delete” icon.

Of course, you can’t do much about letters and cards that you receive by mail other than to ignore and recycle them.

Many real estate agents subscribe to a service which alerts them every time a listing expires on the MLS, and owners of expired listings can expect to be inundated with calls, texts, letters and even door knocks from agents asking if you still want to sell your home and promising to do a better job than your previous listing agent. There’s no way to avoid this onslaught of solicitations. Just know that it’s coming and prepare yourself to say “no” as politely as possible to the live solicitations and to respond that way to text messages and emails. It will only last a few days.

If, however, your listing is “withdrawn” instead of “expired” on the MLS, it’s illegal and unethical for any agent to solicit you. That’s because the definition of “withdrawn” is that your home is subject to a valid listing agreement but merely withdrawn from the MLS. Note, however, that when the expiration date of your listing agreement arrives, the MLS will automatically change your listing status from “withdrawn” to “expired,” and the onslaught of solicitations will begin the next morning.

I don’t want to end this article without assuring you that none of the agents at Golden Real Estate engage in the kinds of solicitation described above. Thanks to our form of advertising (this newspaper column), we depend on prospects contacting us rather than us soliciting you. I myself have been licensed since 2002 and don’t recall ever making a “cold call” or sending a single card or letter soliciting a listing from a homeowner.

Unfortunately, that is unusual in our industry, and I apologize for the behavior of those other real estate practitioners.

The sponsors of the annual Metro Denver Green Homes Tour, held on the first Saturday each October, are preparing to “go virtual” in case an in-person tour is not allowed.

John Avenson’s house at 9988 Hoyt Place, Westminster

That will be accomplished by creating online video tours of the most notable “green” homes featured over the past 20 years. Since I’m on the steering committee for the tour and have the equipment and experience from creating video tours of homes for sale, I volunteered to create those video tours, starting with John Avenson’s home at 9988 Hoyt Place in Westminster.

By clicking here, you can view the 41-minute video tour, led by John, which I created last Friday. It is highly educational.

John Avenson

Many people, myself included, have created homes which can be considered a “model” of sustainability, solar power, and energy efficiency, but John is surely the only homeowner who has turned his home into a classroom for teaching it. He even posted pictures and diagrams throughout the house with instructional content about this or that feature, as you will see on that video.

John’s house was originally built by the Solar Energy Research Institute (SERI, now the National Renewable Energy Laboratory or NREL) in 1981 using then-state of the art technology, but John has diligently, and at great personal expense, kept retrofitting his home with newer technology, which he is happy to explain to visitors and which he explains on the 41-minute video.

CERV monitor screenshot

For example, because of increased insulation and Alpen quadruple-paned windows, he was able to get rid of SERI’s supplemental natural gas furnace, installing a conditioning energy recovery ventilator (CERV) which is powered electrically. His grid-tied solar PV system provides all his home’s energy needs and has reduced his Xcel Energy bill to under $10 per month — the cost of being connected to the electrical grid.

Some of the technological innovations featured in my video with John were new to me. For example, the Alpen windows across from his kitchen have horizontal micro-etching which redirects the sun’s rays 90° upward to his ceiling instead of straight through the glass, reducing the need for lighting.

John provided his email address in the video, saying that his “learning center” is open 24/7 and that he welcomes all inquiries and visitors.

It has certainly been an interesting and emotional two weeks since the murder of George Floyd by a Minneapolis police officer. Rita and I have been happy to add our voices, and are impressed at the longevity and the worldwide spread of the demonstrations.

On Sunday afternoon, there was an event in downtown Golden, which the two of us attended. (See the picture by Chris Davell of Goldentoday.com below.) It was followed by a march through downtown Golden, although Rita and I didn’t stay for that.

The event was organized by a group called Golden United. I have attended several prior events by this wonderful organization, headed by Golden resident Ron Benioff. You will probably read about it elsewhere in this newspaper since I met the reporter covering it. Several hundred people attended the event in Parfet Park, most of them wearing masks and all socially distanced.

It was, of course, very peaceful. After all, this is Golden, a college town that is majority liberal, majority white, and my home for the past 23 years. A city councilor, JJ Trout, emceed the event, giving a very thoughtful speech of her own. Mayor Laura Weinbergalso spoke. Both displayed great introspection and deep thought on the topic of racism. Ron Benioff spoke, stressing that being non-racist is no longer enough. We all have to be anti-racist.

The police chief, Bill Kilpatrick, was there with one other officer and received generous applause at the mention of his sensitive letter to the community which he wrote shortly after the death of George Floyd. (That was followed this week by a lengthy posting on the city’s website outlining police practices and training related to implicit bias, the use of force and other topics raised following George Floyd death.)

I have a couple thoughts to share beyond my sincere appreciation for Golden United and our city’s political leaders.

First of all, I feel that we are overlooking anti-Hispanic racism, which is just as pervasive as anti-black racism. It was the first and remains the greatest expression of racism by our current president, who opposes even legal immigration from people of any color other than white. (Remember his comment about Norwegians being more desirable than Hispanics?)

It’s my perception, and perhaps yours, that whites and the police are not as fearful of Hispanics as they are of African-Americans, but they still don’t view Hispanics as equally valuable human beings.

I certainly value and appreciate our Hispanic population and especially the Mexican-Amercans and their undocumented cousins who work tirelessly and with seeming contentment at so many jobs which other Americans are unwilling to perform — picking our vegetables and fruits, repairing or replacing our roofs, and collecting our trash alongside African-Americans. (It was heart-warming last week to read a post on NextDoor urging neighbors to tape dollar bills to the lids of our trash carts as a way of thanking our trash collectors.)

Not only do we as a white society insufficiently appreciate our black and Hispanic population, our regressive laws work to keep that population impoverished. We need to address our anti-poor policies — which are really pro-wealthy policies, such as the Trump tax bill of 2017 — which have widened the gap between rich and poor in America.

Real estate, at least in the Denver market, is a majority white industry, not representative of the racial diversity of the metro area. I can say with confidence that it’s not reflective of any anti-black discrimination in hiring. My first partner in real estate with whom I co-listed properties was an African-American woman who I miss working with. She remained with Coldwell Banker when I moved to RE/MAX Alliance before starting Golden Real Estate.

My seven broker associates are all white, but they and I would welcome with open arms one or more African-American and Hispanic agents to join our ranks. It is hard to say why our industry has not attracted more African-Ameri-can brokers, but I’ve noticed a large contingent of Hispanic agents, who even have a highly active association. I’ve attended their events.

For this column, I interviewed two of the three blacks who serve on the 18-member board of directors of the Denver Metro Association of Realtors. That ratio, it should be noted, is better than the ratio of blacks who are members of DMAR.

Milford Adams, managing broker of Lyons Realty Group LLC in southeast Denver, told me that economics are the primary reason there aren’t more blacks in the industry, since it’s hard for a new agent to get established in the business without significant cash reserves. (I know this personally, since it was two years of expenses exceeding income before I myself started making a living in real estate.) And, yes, he said he has experienced discrimination, much of it subtle, at every turn as he himself rose through the profession.

Lori Pace, of Kentwood Real Estate in the City Properties office in downtown Denver, has been an activist within the profession and operates a strategic consulting business, offering training to real estate brokerages (see her website, www.LoriPace.com) in the area of recruitment and diversity training. On that website you can also watch her TEDx talk “Philanthroperty,” which was about inspiring women, not just minority women, to invest in “real estate, not purses,” to grow in wealth and power.

The following was submitted by Lori Pace regarding the program she teaches on diversity:

Everyone’s experience matters and how we live, make a living, and lose lives. There is no such thing as a stupid white question, but there is certainly are intellectual black answers. The Diversity Difference is an essential wellness program illustrating how real estate and health equity impact everyone’s ability to breathe or exhale.

The Diversity Tool Kit is THE ventilator allowing everyone the opportunity and right to exist and not resist. It is designed to develop a multicultural, multi-generational mindset. The live and virtual keynote address combines a training series with first-hand accounts and stories on doing business while being Black in America. It is more than a call to action. It is a collaborative, result-driven process tackling multi-layers of problems and resolutions examining metrics, business strategies, and tools for real-life situations. Passive conversations become proactive actions.

This is a resource to ensure strategic, proactive, and sustainable ACTIONS that can be implemented immediately. The agenda is based on an inspirational and REAL approach providing new perspectives for all industries, organizations, and institutions ready to implement a blueprint from a black perspective.

Participants gain a new outlook and opportunity to breakdown and understand how systematic racism in businesses and communities continues to be influenced by the power of segregation and money. Transparency and trusting safe cultures are non-negotiable in order to move forward. The experiential learning deals with Fair Housing and intentional and unintentional Unfair Business Practices. It is time to invest in business, social and emotional “Black and Blue Print” to change your PACE unapologetically with a high return on your investment.

The Real Estate industry and brokerages are major players influencing ALL communities, neighborhoods, business, and institutions. There is a new demand for answers to awkward questions and circumstances requiring a no-judgment solution. Now more than ever, the world is aware of the negative impacts of silence and ignoring the blinders that have been abruptly removed.

The brokers of Golden Real Estate, who are listed below, are among the most knowledgeable and experienced Realtors in the business. Each of us has our own area of expertise and geographic area of service covering the Denver metro area, both in listing homes and helping clients to buy homes. We also have a unique “Lease With a Right to Purchase Program.” In addition, we can refer you to property management and commercial Realtors, since our exclusive focus is on residential real estate.

We welcome the opportunity to earn your business. We have many exclusive services, such as our free moving truck (with free moving boxes) and our live action narrated video tours of every listing, not just unnarrated slideshows or 3D virtual tours. And our commission rates are competitive. Give one of us a no-obligation call!

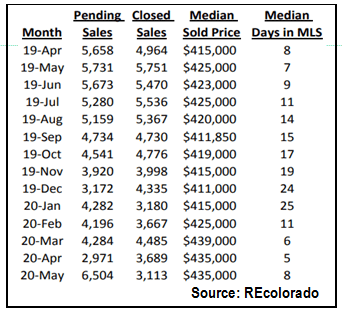

Yes, the Covid-19 pandemic hurt the real estate market in April, but it sure made a rebound in May! The 13-month chart below is for Adams, Arapahoe, Broomfield, Denver, Douglas and Jefferson counties.

Last week and this, you probably heard or read about how bad the real estate market was in April, and that was true here in the Denver Metro area, as it was throughout the country.

Pending sales of new and existing homes in April were roughly half the pending sales of April 2019. But pending sales in May surged to a number that was greater than the number for any month since before 2010, which is as far back as REcolorado’s statistics application goes.

The number of closings in May was somewhat low because of the low number of homes that went under contract in April. The number of closings in any given month is always within range of the number of pending transactions the previous month.

(Note: The number of pending and closed sales for May is from June 1st, It could go up as additional May contracts are reported on June 2nd & 3rd.)

It should be noted that, despite the lower number of pending and closed listings in April compared to 2019, the median sold price was much higher — $435,000 vs. $415,000 in April 2019. The median sold price for May was also higher than the median sold price that month in 2019.

It’s also worth noting how quickly listings went under contract in April and in May. April listings went under contract in 5 days (median figure), which was even faster than last year, while May listings went under contract in 8 days (median) vs. 7 days last year.

These statistics may come as a surprise to those who think that the real estate market is on a downturn because of Covid-19. I am as surprised as anyone at the resilience of our real estate market.

Driving the market is the fact that there is still a low supply of homes for sale and an over-supply of people needing or wanting to buy a home. That explains the low “Days in MLS” figure for April when the number of homes for sale was so low. Because so many sellers postponed putting their homes on the market during the lockdown, it became more of a seller’s market than before. That meant that the homes that were on the market had less competition for the large number of buyers.

Given what we’re seeing now, it’s hard to be pessimistic about the future of our real estate market, however pessimistic we might be about the country as a whole, given the rioting in multiple cities around the country, including Denver. We’ll see in June how much impact that may have.

Another wildcard is the possible resurgence of the coronavirus, given how our state, like others, has yielded to pressure to reopen earlier than CDC guidelines recommended. A resurgence could result in another stay-at-home order.

Accessory dwelling units (ADUs) have been around for a long time. Fonzie lived in one (above the Cunningham’s garage), but they fell out of favor with local governments. Recently, local governments have warmed up to ADUs, promulgating zoning regulations encouraging them, especially detached units in a backyard or above a garage.

You may have heard ADUs referred to as backyard bungalows, micro homes, retirement cottages, guest houses, mancaves, she-sheds, or mi casita. They are created for many reasons: independent living for relatives (aging parents, 20- somethings), rental income/investment property, home office, studio, etc. These days it could be quarantine quarters.

Local governments like them as one way to address the pressing issue of affordable housing in a way that is sustainable, is a compliment to the neighborhood, and provides more affordable housing. People hardly realize they are there, and when they do, often want one.

ADUs have been approved by the state of California, where affordable housing is a crisis throughout the state.

The tiny house movement has popularized the idea of radical downsizing and the concept that living in a small space has many positives. ADU’s are not tiny houses, as the term is used today. ADUs are something more. Although small, they are a complete living unit with a full kitchen and bathroom, with a comfortable living area suitable for entertaining. They have a foundation and meet all code requirements. ADUs are more expensive than tiny homes, but they can be worth it.

How much do they cost? Pre-designed manufactured (built off-site) units can be less than $200,000, and even less depending on the characteristics of the site and choices made by the owner.

Would you like to know more? A good resource is at www.AccessoryDwellings.org, created by Kol Peterson. Peterson lives in Portland, Oregon (an early adopter of ADUs), has built many himself, and conducts workshops on all aspects of the process.

ADU above a garage

Locally, a company called Verdant Living sells manufactured ADUs, not ones that are “stick-built” on-site, so if that works for you, you can email them at bungalow@verdantliving.us for more information. They can refer you to other companies which build ADUs, whether free-standing, over your garage, or in a walk-out basement.

Personally, I have sold homes which have ADUs. Having a rentable unit can make a home more affordable to many buyers.

One reader said they were offered a quick sale of $120,000 cash, but called me before agreeing to the transaction. My research showed their home could sell for twice that amount.

I wasn’t contacted in time to save an elderly Arvada couple from being coerced into selling their home for half its worth by a developer who made a point of telling the couple not to tell anyone about their transaction. The couple actually felt threatened, not just coerced. Indeed it was a neighbor who told me about the transaction, because the couple still felt obliged not to reveal anything.

Call me if you have been approached by an investor urging you to sell your home for what sounds like a good price. I’ll tell you if it really is — or if you should get more money for it. Write to me at Jim@GoldenRealEstate.com or call me at 303-525-1851.