We all realize by now that the real estate market is slowing due to a reduced buyer pool, caused in part by the increase in mortgage interest rates.

Here’s some advice to sellers who don’t want their home to sit unsold on the market.

1) Reconsider buying your replacement home first, expecting to sell your home immediately. That strategy was based on the difficulty in finding a replacement home. Now you can sell first, have a 45- to 60-day close and reasonably expect to find your replacement home before you have to surrender your current one.

2) Don’t price your home based entirely on recent comparable sales, but price it slightly lower. Buyers know the market is softening and will be looking for a good deal.

3) With an increased inventory of listings, it’s more important than ever to stage your home and improve its curb appeal as well as its interior appeal.

4) Listen to the market. If you get few showings and no offers in the first week, don’t wait to lower the price.

5) Magazine-quality pix and video are more important now to make your home stand out. Hire an agent who will order professional HDR still photos, shoot a narrated video tour and drone video, and market your home the way Golden Real Estate does.

When interviewing a listing agent, ask him or her to bring their Matrix productivity print-out instead of trusting their verbal description of their level of success with prior listings.

In Colorado, property taxes are based on a calculation of what each property might have sold for on June 30th of the prior even-numbered year.

That means the property taxes for 2023 and 2024 will be based on what your home could have sold for on June 30, 2022. Given the crazy surge in home prices, you could see a 30% or higher jump in your property’s assessed valuation and therefore a 30% or higher jump in your property taxes for the next two years.

The chart below shows the likely impact of the current run-up in median prices compared to the median prices in prior Junes of even-numbered years, based on data from REcolorado. Although your home’s valuation will be based on the sales of comparable homes near yours leading up to June 30, 2022, the fact that the median sold price of residential properties metro-wide will have increased by over 30% from June 30, 2020, suggests that your home’s valuation and therefore your taxes could rise by 30 percent or more.

I’ve estimated (conservatively) that the median sold price in June will be $570,000 because the median sold price was already $540,000 in February. That is already a 27.7% increase over June 2020.

That, however, is an average for the entire Denver metro area, defined for these purposes as within 25 miles of the state capitol. There are locales within the metro area where the increase in values over the last two years have approached 35% or more. Here is how that metro-wide 27.7% average increase of Feb. 2022 over June 2020 breaks down by county:

Denver County—19.5%

Jefferson County—30.1%

Douglas County—31.9%

Adams County—28.6%

Arapahoe County—27.1%

Boulder County—40.7%

Gilpin County—42.4%

The appreciation also varies greatly by city addresses:

Golden addresses—15.9%

Littleton addresses—26.0%

Arvada addresses—33.0%

Broomfield—27.2%

Centennial—36.9%

Aurora—30.5%

Highlands Ranch—31.8%

Castle Rock—36.5%

So, keep an eye on what homes like yours are selling for this April, May and June of this year to get a sense of what the county assessor’s valuation of your home will look like when you get that notification in May 2023.

About 50 readers are receiving “neighborhood alerts” from me. These are email alerts regarding all MLS listings within your particular neighborhood. Usually, the alerts cover a certain subdivision or ZIP code, but they could be structured to include only listings which are comparable to your own home. For example, if you have a 1970s ranch home, I could set up an alert that only includes ranch-style homes built between 1960 and 1990 within a half mile or mile of your home. This will give you the best indication of how the value of your own home may be calculated by your county assessor. Feel free to email me at my address below to request such an alert or to modify the alert I am already sending you.

One of the most dependable indicators of a strong “seller’s market” is the number of listings which sell above their listing price, and by how much. Another is the number of days that a listing is on the MLS (“DOM”) before going under contract.

As shown in the chart below, drawn from REcolorado’s data for the period of January 2021 through last month, the seller’s market peaked in May and June of last year but has now surged again. All indications are that the surge will continue through the spring.

Average DOM is always higher than median DOM because there are many homes that languish on the market unsold because they are overpriced, or for another reason. What’s remarkable about this sellers market was how low the average DOM went as even those hard-to-sell homes attracted buyers.

As with the previous surge, the average DOM has sunk below 20 while the median DOM has revisited its all-time low of 4 days on the MLS.

(Note: These statistics are for residential listings in the metro Denver area, which I’ve defined here as within a 25-mile radius of the State Capitol.)

The rising cost of money — that is, the increase in mortgage rates projected for this year — will lure many buyers “off the fence” hoping a buy a home before interest rates rise further.

I foresee a stronger than usual seasonal jump in the number of new listings as spring arrives.

Many people believe, erroneously, that the best time to list a home is in the spring, so those people will be putting their homes up for sale in the coming weeks. In addition, as I wrote last week, many homeowners who weren’t thinking of selling before are likely to decide it’s a good time to “cash out.” But I don’t foresee that increase in supply going far to meet the needs of today’s home buyers, and I don’t see prices leveling off, much less declining.

It surprises many of us that homes are appraising at the high prices they are selling for, but when a winning bidder waives appraisal objection to win a bidding war — which is almost common nowadays — that sale becomes a comp that supports future appraisals at the same price or higher. (On the appraisal form, there’s a place to indicate a rising, falling or stable market, and when an appraiser checks the box that it’s a rising market, that gives him or her more leeway to appraise a home higher than recent comparable sales might otherwise justify, further fueling the frenzy.)

The real estate market is becoming less and less predictable, along with other elements of our economy and society. War could be imminent or a new Covid variant might come. God only knows!

Rita and I are both 74 years old, and, although I have no plans to retire at this time, we have decided for various reasons to sell our home and move into a 55-plus community. Knowing that many of my readers are seniors, I’ve decided to share some of our thinking.

When you’re our age, you can’t predict when you might have to sell, so I have always recommended that seniors do it while they can instead of waiting until they have to. It is also kinder to your heirs to downsize possessions yourself rather than leave that task to them after you die.

The run-up in home prices has been breathtaking, hasn’t it? It’s difficult to predict how much longer it will last, but Rita and I do know that we can be satisfied with the proceeds we will get from selling our home now. The income from those proceeds in a TransAmerica fund that guarantees a certain return despite market fluctuations would help pay the rent for our new apartment. And, since I’m not retiring yet, I’ll continue to have an income on top of that.

Social Security, Medicare and appropriate long-term care policies for each of us can provide additional peace of mind regarding our medical needs as we age.

Our decision to move into a 55-plus community also relieved us of the biggest dilemma facing homeowners who want to capitalize on selling their current home — how to find a place to buy in a very difficult market for buyers.

While it’s nearly impossible and highly frustrating to buy in this crazed seller’s market, and while the renter’s market is also extremely tight and expensive, there are many 55-plus communities like the one we chose that have units available. In addition, it’s the nature of these places that openings become available as other residents die or move into assisted living facilities.

You’ll want a professional to help you evaluate the different 55-plus communities that exist and that are opening every year. Some, like the one we chose, are straight rentals, but others require a 6-figure “buy-in” which can eat up the proceeds from the sale of your home. I suggest hiring Jenn Gomer, who is in the business of helping seniors find the community which is a right “fit” for their specific needs. You don’t pay Jenn for that service — she receives a fee from the community you select.

The dilemma mentioned above is solved by waiting until you have signed a lease on your rental (ours starts on April 1st), then putting your home on the market with a closing date 15 days after your lease begins. That way you have a reasonable amount of time to move into your rental (using Golden Real Estate’s free moving truck, free moving boxes and affordable laborers, if you listed with us). It also gives you time to dispose of your excess “stuff.”

It has been an interesting if exhausting process to let go of the family heirlooms, mementos, and other possessions that have slowly filled our unfinished basement over the years — stuff that we have lugged from one house to the next.

The Marshall fire had a psychological impact on us, too. We imagined if our own home were to be consumed by fire unexpectedly and we had to start over, losing everything we enjoy daily as well as all that stuff in our basement that we have been dragging along each time we bought a new home. Would we miss it? Of course, but we could live without it, couldn’t we?

There’s a freedom to be gained by releasing the past and living solely in the present. It felt good giving away things to Goodwill and other charities as well as to friends and relatives.

For example, since acquiring an electric bicycle several years ago, the three conventional bicycles we owned had been sitting unused in our basement and were never likely to see the light of day again. So we donated them, along with bicycle parts and accessories such as paniers and pumps, to the “Bicycle Recycle” program of the Golden Optimists Club, which refurbishes bicycles and donates them to low-income people. Making that donation felt great, on top of the feeling we got from clearing them and other stuff from our basement.

We thought about giving most of our furniture to victims of the Marshall fire, but realized that an estate sale was more practical and then we could donate money instead. Except for a few pieces, we’ve decided to purchase all-new furniture for our 2-bedroom/2-bath apartment at Avenida Lakewood.

It’s amazing how many papers were in boxes in our basement. I found tax returns going back to the 1980s which needed to be shredded. We also had the closed transactions of Golden Real Estate going back well beyond the number of years we’re required to retain them, and we were able to move the more recent transactions to the company’s new office in downtown Golden.

We had carpet remnants for carpeting that no longer existed at home and office. Bye-bye! We took multiple carloads of nice things that we didn’t need to Goodwill, which thankfully accepted all of it.

The wheelbarrows and gas generator that we never used but lent to Habitat for Humanity for its pumpkin patch each October are now in that organization’s own storage facility, not in our basement.

Anyone want to buy our really sweet upright piano?

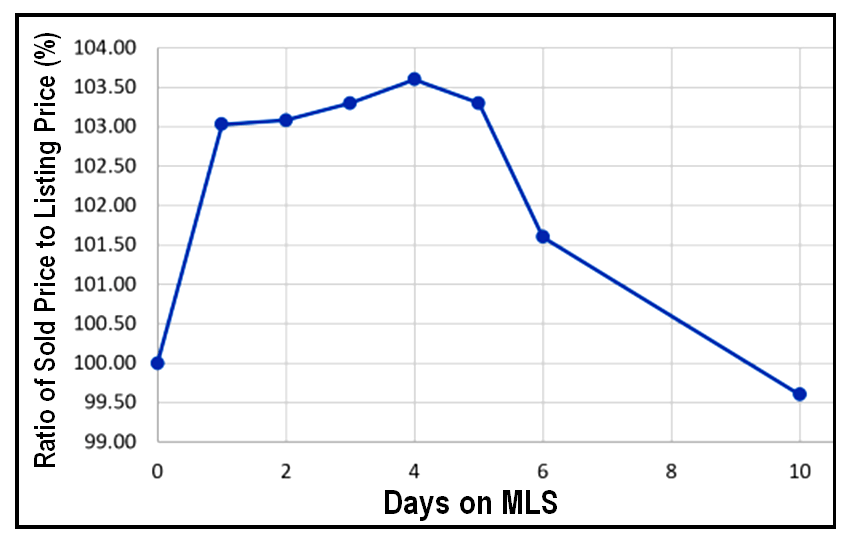

I have written before that 4 days on the MLS is the right amount of time to get the highest price for your home. That was based on an analysis I did several years ago, so it’s time to do a new analysis.

Looking at the 4,015 most recent sales in Jefferson County, here’s what I discovered.

Roughly 5% of those sales showed zero days on the MLS, meaning that they weren’t even exposed to agents or the public until they were under contract. The median ratio of sold price to listing price for them was 100%. Some sold for over the listing price and some for less, but the median was the listing price.

Meanwhile, 200 homes went under contract after being on the MLS only 1 day. The median home for this group sold for 3.03% over its listing price.

There were 379 homes that were active on the MLS for 2 days before going under contract. The median home in that group sold for 3.08% overits listing price.

502 homes went under contract after 3 days on the MLS. The median home in that group sold for 3.3% overits listing price.

The highest number of homes, 608, were active on the MLS for 4 days before going under contract. The median home in that group sold for 3.6% over its listing price.

As in my prior analysis, being on the MLS for 4 days netted the highest price for the seller.

413 homes went under contract after 5 days on the MLS. The median home is that group sold for 3.3% overits listing price.

Another 206 homes went under contract after 6 days on the MLS, but the median home in that group sold for just 1.6% overlisting price.

Skipping ahead to the homes that were on the MLS for 10 days before going under contract, the median home in that group sold for 0.4% belowthe listing price.

Those statistics are displayed graphically on the chart above. Not shown in that chart is how low the ratio of sold price to listing price went for homes that languished on the market, usually because they were overpriced at the beginning. Here’s that other data:

223 homes were active on the MLS for 30 to 45 days before going under contract, and the median home in that group sold for 3.8% below the listing price. Looking at the 106 homes that were active on the MLS for 46 to 60 days, the median home in that group sold for 4.3% below listing price.

Lastly, 285 homes were active on the MLS for over two months. The median home in that group sold for 5.7% below the listing price.

The lesson for sellers is that you need to price your home to attract multiple offers and not accept the first (or second) good offer that you receive. Four days is the right amount of time, with proper marketing, for all potential buyers to learn about your home and enter the competition for it.

Selling it without making it active on the MLS at all, as too many sellers are currently doing, may be convenient, but it likely leaves money on the table.

There’s another way that sellers leave money on the table, and that is to hire a listing agent who uses the “highest and best” approach to handling multiple offers. It is the most common method used, but the agents of Golden Real Estate use a better approach — being open and transparent, handling bids auction-style.

The auction style of handling multiple offers is simple, but it does require more work by the agent and more patience on the part of the seller. Buyers and their agents appreciate this approach — and sellers are likely to net more money.

I have a good example from last week. I listed a home for $595,000 and got it under contract for $725,000, and I did it with only four bidders. If I had asked for “highest and best,” I would have had many more offers, and maybe the highest and best would have been $625,000 or maybe $650,000. But because I let every agent know the details of every offer I received, I received fewer offers, and those I did receive knew when their offer was exceeded by another offer. At that point they could either resubmit or drop out.

This process truly resembles a public auction, in which everyone knows where they stand and can choose to raise their bid or drop out. No one is blindsided. The worst thing for a buyer is to discover later that if they had only offered a little more money they could have purchased the home they wanted.

It’s hard for me to understand why listing agents won’t reveal their highest offer to other agents. There is no rule against it, but some agents seem to think there is. Some agents claim that their seller doesn’t want them to reveal details of the offers in hand, but I don’t believe that. And if it’s true, then the seller wasn’t told about the advantages of the auction style of managing offers.

If you want to get the most money for your home, use an agent like those of us at Golden Real Estate who are willing to do the extra work of handling multiple offers auction-style.

Basically, iBuyers such as Opendoor and Zillow Offers attempt to lure homeowners in-to selling their home for what appears to be a good price but which is literally intended to net the seller less than if they exposed their home to the full universe of potential buyers.

Literally intended? Yes, all you need to know is that if a company wants to buy your home in order to resell it, it’s because they will make a profit from doing so. Wouldn’t you want to keep that profit for yourself?

Now Zillow has weaponized its much criticized “Zestimate” for the purpose of getting their “foot in the door” with you. Let me share with you a few points to ponder before responding to Zillow’s pitch.

First of all, you and I both know that the Zestimate is a computer-generated number that is by definition not particularly accurate. (Zillow’s estimate on my own home is at least $100,000 over its true value.)

To facilitate their iBuyer program in Colorado and elsewhere, Zillow made big news recently when they opened brokerages and started hiring brokers. They have opened an office in Centennial and, as of this week, have 15 broker associates, 12 of them members of the Denver Metro Association of Realtors. The others belong to an out-of-state Realtor association. So far that brokerage has put zero listings on REcolorado, our MLS, whether active, pending or closed. Presumably those 15 broker associates are busy responding to homeowners who responded to Zillow’s pitch about buying their home for the Zestimate price. How will those meetings go?

First, the broker associate will do a true market analysis and explain that the Zestimate was computer generated and overstated their home’s value. “Here’s what we will offer you, now that we know the true value.”

If the seller accepts the lowered price and signs a Zillow purchase contract, it will have the following provisions, assuming it’s similar to the contract from Opendoor that I was able to study.

First of all, the seller will have accepted a 7½% “service fee” in lieu of a commission. Next, they will have agreed to an inspection or “assessment” of the property, which will be followed by “adjustments” to the purchase price based on “needed repairs,” including, for example, a new roof, a new furnace or water heater based on age — whatever can be justified. The example I cited in my August 2019 column mentioned $38,563 worth of “repairs found in assessment.”

That contract had an escape clause for the seller, which Zillow’s contract probably does too, allowing the seller to terminate at any time, which is what that buyer did. The combination of the “service fee” and the reductions to cover supposed “repairs” was so great that they called me. I listed their home for the right price and sold it above asking price due to multiple offers, netting the seller more than they would have netted under their contract with Opendoor.

I got the seller more money, because, as I said above, the only reason for Opendoor or any iBuyer to purchase a home is to sell it at the market, which requires them to purchase the home below its market value.

In the iBuyer marketplace, Zillow clearly has the advantage, because virtually every homeowner is already being dazzled by the Zestimates they get routinely by email, whereas Opendoor and other iBuyer competitors have to canvass and cold-cold homeowners about selling their home “without putting it on the market or paying a commission.” Zillow enjoys what every brokerage wants — sellers calling them! All the Zillow brokerage has to do is employ enough agents to answer the phone and arrange those in-home “selling” appointments, which are really for the purpose of listing the home for sale once it is owned by Zillow.

It’s a great business model — for Zillow, but not necessarily for the homeowner. That is, unless the homeowner is willing to give up thousands of dollars in proceeds in return for the “convenience” of selling without any showings or other intrusions.

For some homeowners, that convenience is worth the loss of proceeds, and there are probably enough such homeowners to make the iBuyer model successful. What bothers me is that for some it will feel like a “bait and switch” situation. After all those “adjustments” have been made, they might be un-able or unwilling to exercise their right to terminate the contract because they have made life plans based on the expectation of selling their home for an acceptable price.

Some will have already signed contracts for a new home or at a senior community. They will have already packed some of their belongings or put them in storage, and they may have told their friends that they are selling and moving. For these persons, it may be psychologically difficult or financially costly to reverse course when they discover they have been fooled into selling their home for less than its worth.

If you have responded to the Zillow pitch and would be willing to share your experience, I’d like to hear from you. My email address is Jim@GoldenRealEstate.com. I’ll share what I learn in a future column. Subscribe to this blog to get alerts about future postings on this or another topic of interest.

Perhaps you’ve heard about the new concept in home selling called iBuyers. Open Door, Zillow Offers and OfferPad are offering this way of selling your home. Basically, these firms use their own cash to buy your home and then re-sell it for a profit.

If you’re a seller who needs to sell quickly and you’re not worried about getting top dollar (or paying less in fees), the iBuyer model is an option that may not otherwise be available to you. You avoid the uncertainty of not knowing how long your home will sit on the market — or whether it will sell at all.

A company called Collateral Analytics has published a study of 4,000 iBuyer transactions in Phoenix which outlines the costs to sellers and the earnings vs. risks for these iBuyer companies. The report’s title is “iBuyers: A new choice for home sellers, but at what cost?” It was released two weeks ago. To read the full report, click on this link.

The last paragraph in the report is a good summary of their findings: “These preliminary empirical results suggest that sellers are paying not just the difference in fees of 2% to 5% more than with traditional agencies, and a generous repair allowance, but another 3% to 5% or more to compensate the iBuyer for liquidity risks and carrying costs. In all, the typical cost to a seller appears to be in the range of 13% to 15% depending on the iBuyer vendor. For some sellers, needing to move or requiring quick extraction of equity, this is certainly worthwhile, but what percentage of the market will want this service remains to be seen.”

In May I got a call from a couple which was under contract with OpenDoor for $548,500, but with a 7% “service charge” and $38,563 for “repairs found in assessment.” This way of doing business annoyed them enough that they terminated with OpenDoor and listed with me at $498,000, selling for $507,000, which netted them more.

Above is one of 3 charts in the report. The analysis is from Phoenix, where OpenDoor began buying homes in 2016, because they didn’t come to Denver until 2018.

I’ve written in the past about companies which will buy your home “as is” for cash without putting it on the MLS. Then they flip the property to a new buyer for a profit — profit that you gave up by doing business with them. The same is also true with iBuyers.

Bottom line: Unless money is no object for you, you’ll do better listing your home with a full-service traditional brokerage like Golden Real Estate. Call any of us at the phone numbers below!