With everything costing more these days, from groceries to gasoline to natural gas, what is the effect on the real estate market?

No doubt, you’ve heard that the year-over-year consumer price index increased by 6.8% in November, the highest increase in 40 years.

You also know that real estate prices and rents have increased too. So how do those statistics compare, and is buying still a better choice than renting?

Home prices have actually increased more than consumer prices over the last year, making real estate ownership the best hedge against inflation. In the Denver metro area (excluding Boulder) as of Sept. 30, 2021, according to the National Association of Realtors (NAR), the average sold price of homes was $614,800, an increase of 21.5% over the prior year. The average apartment rental price was $1,689 per months, an increase of 12.5% over the prior year. If you had a mortgage, the average monthly cost of ownership of that average home purchase was an astounding $4,126 per month for a single family detached home, making the rental of an average apartment much more affordable.

But, of course, the money you spend on rent is money down the drain, whereas the homeowner may find that the value of his/her home increases by more than the monthly mortgage payment. To me, there’s no comparison to owning vs. renting, but I understand that renting makes sense for many families.

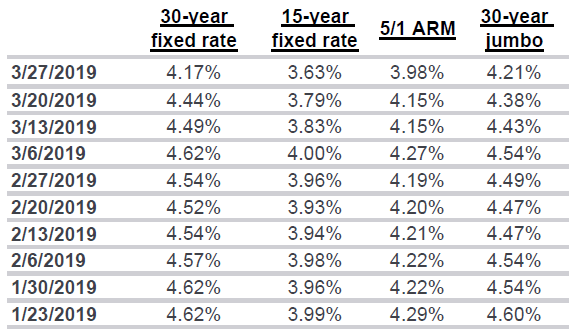

So, what’s the prognosis for home ownership in 2022? Because of the inflation rate, we can also expect mortgage rates to rise from around 3% to 3.7% in 2022 according to NAR, but if you already own your home, your low interest rate is locked in. Mortgage rates currently average 3.1%, according to Freddie Mac.

A higher interest rate, however, could affect what you might sell your home for, if that’s in your plans. Compared, however, to the increase in value you’ve already experienced, I don’t think the effect of higher interest rates will be too much of a downer for you, should you choose to sell.

Unless you’ve switched to heat pump heating and cooling and have installed solar panels to generate the electricity, your home heating cost will increase in 2022. The cost of natural gas has already increased by 25%. The nice thing about electricity is that its cost can only increase by a vote of the Public Utilities Commission, and those increases are more gradual.

Gasoline costs have skyrocketed, but, again, the electricity to power EVs has not, and if you installed enough solar panels, you probably pay nothing for your car’s fuel. I suspect that solar installers are doing a good business nowadays. The cost of solar has plummeted, so call an intaller for a quote.