If you follow mortgage interest rate fluctuations, you may wonder how mortgage rates can drop despite several increases in the Federal Reserve’s much talked about discount rate over the past year.

The benchmark 30-year mortgage rate plummeted 27 basis points (over 1/4 percent) last week, the biggest weekly drop in a decade, creating a huge affordability window for home buyers and for homeowners considering a mortgage refinance. The last time the benchmark 30-year rate was below this level was Jan. 3, 2018, when it hit 4.10 percent, according to Bankrate’s historical data.

This can be a teachable moment, so I asked one of my preferred lenders, Scott Lagge of Movement Mortgage to explain.

According to Scott, financial markets are complex, and many factors impact interest rates. What we are experiencing currently is based to a large degree on consumer sentiment. As consumers, we can have a huge impact on the market based on what we “feel” about where the economy is headed. If we “feel” the market is getting worse, we hold onto our money, spend less, buy less, and shift our investments from short term to long term investments. Therefore, worries about slowing economic growth can change our behaviors as consumers and as investors. Investors worried about the economy slowing in the short-term start to shift their money to long-term investments such as bonds, specifically mortgage backed securities (also known as mortgage bonds). This flood of money into mortgage bonds reduces mortgage bond values and rates fall due to an over abundance or supply of bonds. In essence, it’s supply and demand.

For a more technical explanation, Scott cited this statement from Greg McBride, CFA, Bankrate’s chief financial analyst: “Worries about slowing economic growth — both domestically and abroad — and the inversion of the Treasury yield curve put investors into semi-panic, bringing bond yields still lower after the Fed indicated no more rate hikes in 2019.”

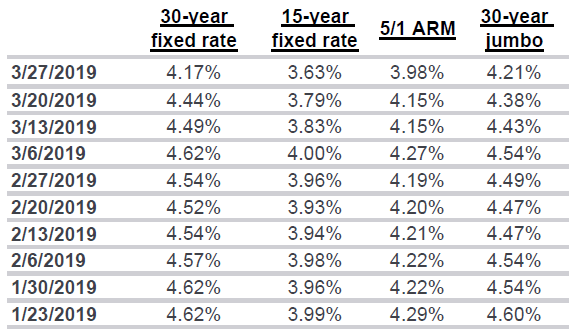

Above is a chart from www.Bankrate.com showing last week’s sudden drop in mortgage interest rates.

Changes in mortgage rates can affect home prices. To the extent that buyers use mortgage financing, what they can afford to purchase goes up or down. As mortgage rates flirted with 5%, we saw a definite softening of the long-running seller’s market. If these low rates last into the coming weeks, we may see more buyers wanting to resume house hunting and lock in a low mortgage rate.

Scott Lagge invites you to call him at 303-944-8552 if you’d like to see what interest rate you qualify for. Call me at 303-525-1851 if you’d like to go house hunting!